The roof section of the 4-point inspection is the one that causes the most anxiety for homeowners, and for good reason. It is the section most likely to result in an Unsatisfactory finding, and when it does, the cost to correct the issue — a partial or full roof replacement — is significantly higher than fixing a double-tapped breaker or adding a TPR discharge pipe to a water heater. Insurance carriers assign specific life expectancy benchmarks to different roofing materials, and a roof that has exceeded or is approaching the end of its expected lifespan will be scrutinized closely.

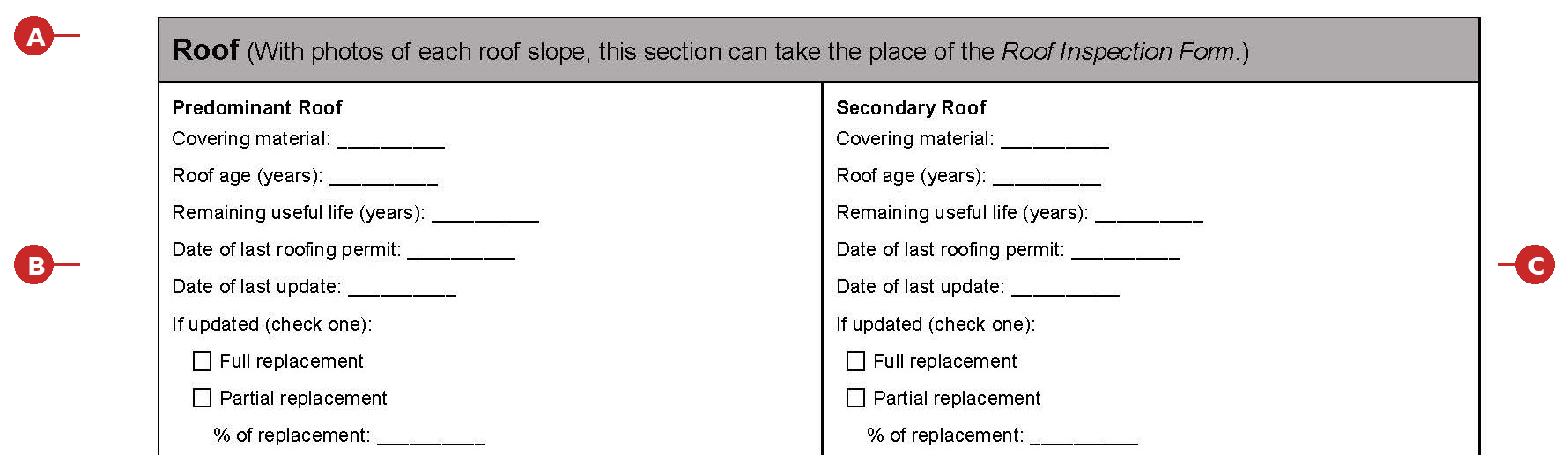

A — Roof Header: “This section can take the place of the Roof Inspection Form”

The note in the header explains that this section of the 4-point form, when completed with photographs of each roof slope, can serve as the roof inspection on its own — replacing the need for a separate standalone roof inspection form. In practice, most inspectors complete this section as part of the standard 4-point inspection, and most carriers accept it without requiring an additional roof-specific form. The key requirement is that photographs of every slope of the roof must be included with the report.

B — Predominant Roof / C — Secondary Roof

The form provides two columns because many homes have more than one type of roof covering. In Southwest Florida, it is common to see a home with a shingle roof over the main structure and a flat or built-up roof section over a lanai, addition, or garage extension. Each roof section is documented separately.

For each, the inspector records the covering material — asphalt shingle, concrete or clay tile, metal, flat or built-up, and so on. The roof age is entered in years, and the inspector estimates the remaining useful life, also in years. These two numbers are the ones the underwriter will focus on most closely. Insurance carriers use general benchmarks for how long each material should last: roughly 15 to 20 years for standard three-tab asphalt shingles, 20 to 25 years for architectural (dimensional) shingles, 25 to 40 years or more for concrete or clay tile, and 40 years or more for metal. A roof with fewer than five years of estimated remaining useful life will almost certainly result in the carrier requiring replacement before issuing or renewing coverage.

The date of last roofing permit and date of last update document the history of the roof. If the roof has been replaced or repaired, the inspector indicates whether it was a full replacement or a partial replacement, and if partial, what percentage of the roof was updated. A partial replacement — sometimes called a re-roof of a specific section — is common after storm damage, where only the damaged area is repaired rather than the entire roof being replaced. The percentage matters because a carrier may view a 30% partial replacement differently than a 90% replacement that is essentially a new roof.

If your roof has been replaced and you have the permit documentation, make sure the inspector has access to it. Permits can typically be verified through your county or city’s public records portal, but having the paperwork on hand eliminates any ambiguity about when the work was done and whether it was performed under permit.

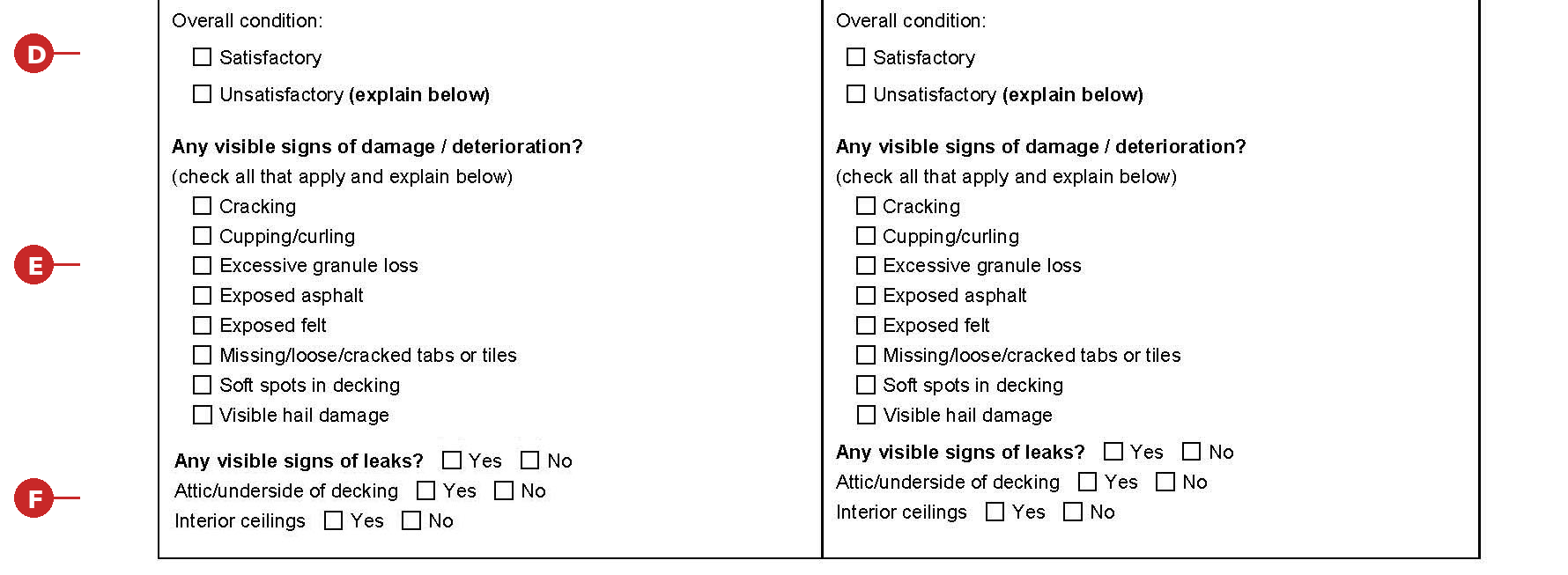

D — Overall Condition: Satisfactory or Unsatisfactory

Just like the other three systems, the roof receives an overall condition rating. A Satisfactory rating means the inspector found the roof covering to be in acceptable condition with adequate remaining useful life. An Unsatisfactory rating means there are conditions present — age, damage, deterioration, or active leaks — that the inspector has determined make the roof unacceptable in its current state. As with every other section of this form, an Unsatisfactory rating here means the insurance company will require the issue to be addressed before they will accept the report.

It is worth noting the intersection of Florida law here. As discussed on the main page of this site, Senate Bill 2-D (2022) established that insurance companies cannot refuse coverage solely because of roof age if the roof is less than 15 years old. For roofs 15 years or older, the insurer must allow the homeowner to obtain an inspection demonstrating at least five years of remaining useful life before they can require a replacement as a condition of coverage. This does not override an Unsatisfactory finding based on actual damage or deterioration — it specifically addresses situations where age alone is used as the reason for denial.

E — Visible Signs of Damage or Deterioration

This checklist covers the specific types of roof damage the inspector evaluates, and the form instructs them to check all that apply and explain below. Each item on this list represents a different stage or type of roof failure, and understanding what they mean can help you make sense of what ends up on your report.

- Cracking refers to splits or fractures in the roofing material — on shingles this often appears as lines running through the surface, on tile it may be visible cracks in individual tiles.

Cupping and curling are deformations in asphalt shingles where the edges turn upward (cupping) or the corners lift and curl away from the roof surface. Both indicate that the shingle is drying out and losing its flexibility, which means it is nearing the end of its useful life.

Excessive granule loss is specific to asphalt shingles — the small embedded granules that protect the asphalt from UV exposure wear off over time, and once enough are gone, the underlying asphalt is exposed to direct sunlight and deteriorates rapidly.

Exposed asphalt and exposed felt represent progressively worse stages of the same problem — the protective layers have worn away to the point where the structural layers beneath are visible and unprotected. - Missing, loose, or cracked tabs or tiles is self-explanatory — any roofing material that is no longer in place or no longer intact creates an entry point for water.

Soft spots in decking indicate that the plywood or OSB sheathing beneath the roofing material has been compromised by moisture — the wood has begun to rot and is no longer structurally sound. This is a serious finding because it means the damage has gone beyond the surface covering and into the roof structure itself.

Visible hail damage documents impact marks or denting from hailstones, which is more common in some parts of Florida than others but is checked for regardless of location.

F — Visible Signs of Leaks

The final portion of the roof section asks whether there are visible signs of leaks, and breaks this question into two specific locations: the attic or underside of the decking, and interior ceilings. These are two different things the inspector is checking.

In the attic, the inspector looks at the underside of the roof decking for water stains, discoloration, daylight showing through, or active moisture. On interior ceilings — particularly in rooms directly below the roofline — the inspector looks for staining, discoloration, bubbling or peeling paint, and soft or sagging areas that would indicate water has made its way through the roof and into the living space. Evidence of leaks in either location is documented and photographed, and will factor into the overall condition assessment.

[Return to the main “Understanding the 4-Point Inspection Form” page]